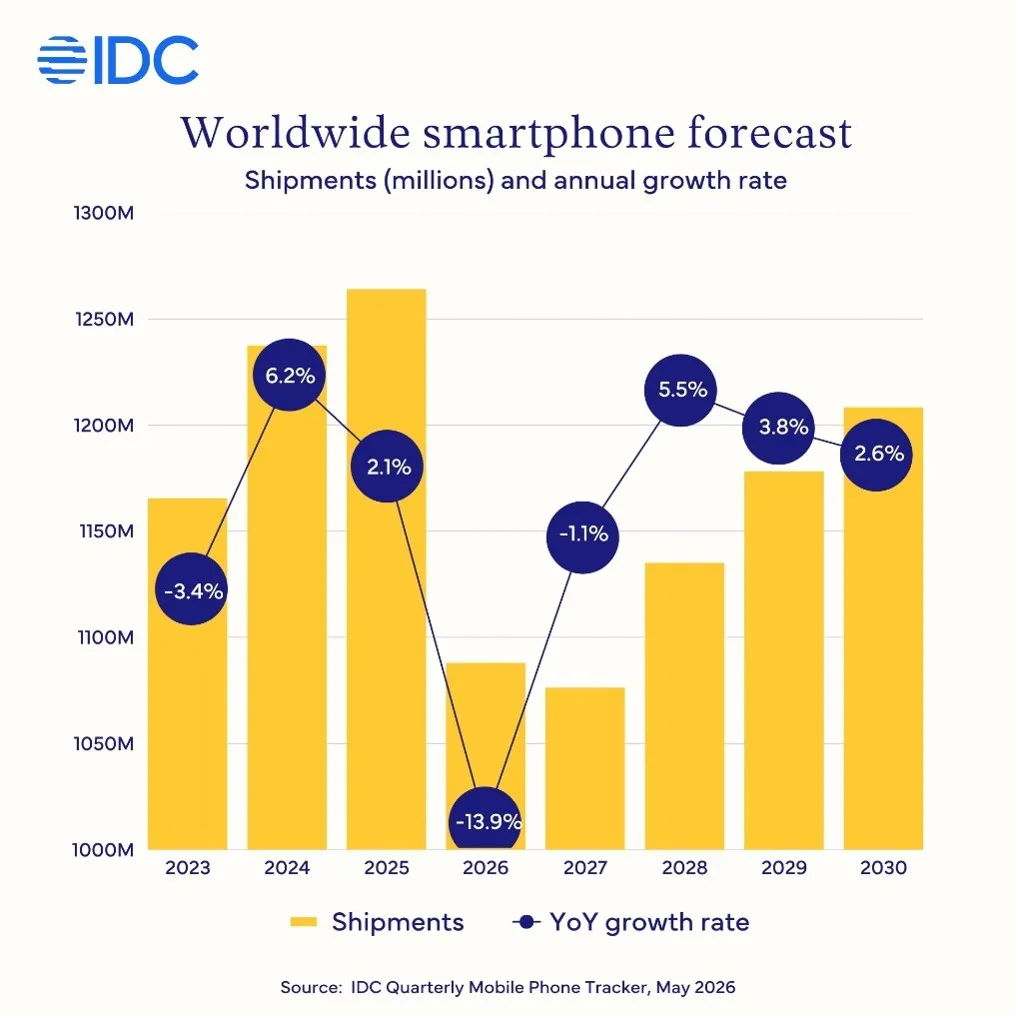

Worldwide smartphone shipments are forecast to fall 13.9% in 2026 to 1.09 billion units, according to IDC. That would mark the market's steepest annual decline on record.

The latest outlook is a further cut from IDC's earlier projection of a 12.9% decline. The researcher now expects the downturn to continue into 2027 with a further 1.1% fall, before a 5.5% rebound in 2028 as memory supply conditions improve.

The revised forecast points to a market under pressure from two forces at once. The memory shortage that began affecting the sector in 2025 remains the main driver, while the US-Iran war has added to manufacturers' costs through higher oil and transport prices.

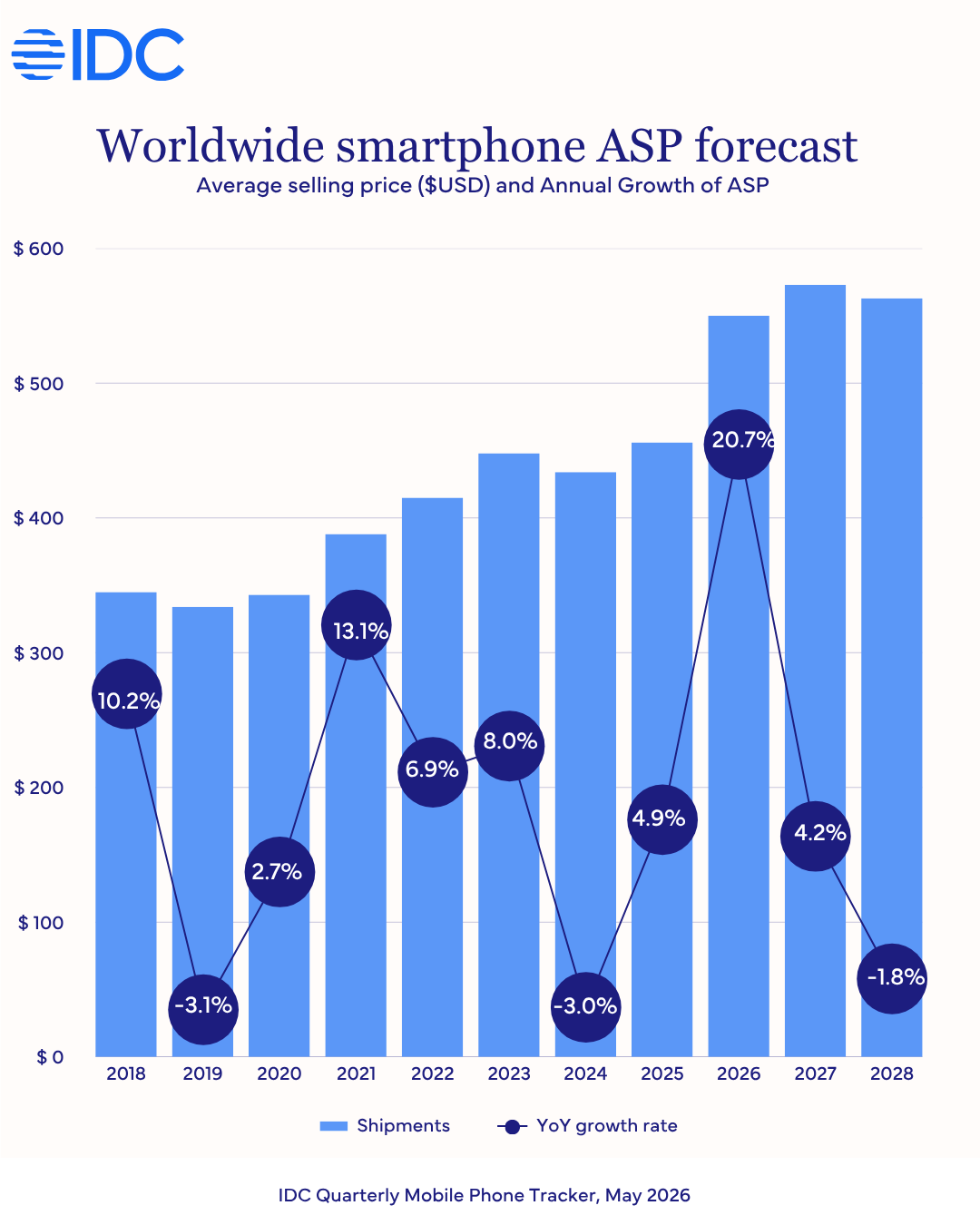

Those pressures are forcing smartphone makers to ship fewer devices and focus on more expensive handsets. Average selling prices are expected to reach a record USD $550 in 2026, up USD $100 from the previous year.

That shift is hitting the lower end of the market hardest. The sub-USD $200 segment is expected to contract most sharply, reflecting weaker consumer affordability and tighter vendor margins.

Emerging markets are set to bear much of the decline. IDC forecasts shipments in the Middle East and Africa will fall 23%, while Central and Eastern Europe will drop 19% and Asia Pacific excluding Japan and China will decline 14%.

By contrast, North America is expected to prove more resilient, with a 6.3% decline. The region is more heavily weighted toward premium smartphones, with 60% of shipments in the first quarter of 2026 priced above USD $800.

China is also expected to post a double-digit decline, with shipments down 13%. Lower-priced Android brands in the country are struggling to compete as cost pressures reshape the market.

Platform split

Across operating systems, Android is forecast to record a 20% year-on-year decline in 2026. IDC said the figure masks a widening divide between larger suppliers with access to components and smaller brands exposed to entry-level price bands.

Samsung is expected to increase market share despite the broader Android downturn. IDC said the company has benefited from secured memory supply, a stronger premium line-up and a push into mid-range devices that smaller rivals cannot match.

Apple's position appears stronger than previously expected. IDC improved its 2026 forecast for iOS from a decline of 8.1% to 5.2%, helped by early memory procurement and demand for the iPhone 17 range in developed markets and China.

"2026 will be a defining year for Apple," said Francisco Jeronimo, Vice President for Worldwide Client Devices at IDC. "In a year when the broader smartphone market will record its steepest decline in history, iOS will deliver its highest annual share ever, at 22%. Apple has done three things that few of its competitors have managed: it secured memory supply early, it built a portfolio strong enough to drive a remarkable turnaround in China, and it positioned the iPhone 17 to capture demand exactly when consumers in developed markets are extending replacement cycles and trading up. The shift in market share that follows from this crisis will benefit Apple more than any other vendor."

IDC also expects HarmonyOS to outperform the wider market. Shipments running Huawei's operating system are forecast to reach 62 million units in 2026, well above the previous estimate of 42 million.

Huawei has expanded HarmonyOS into lower-priced models while holding or cutting prices on new devices and maintaining support for older ones, IDC said. The approach is gaining traction in lower-tier Chinese cities as rising Android prices create room for a domestic alternative.

Cost reset

The forecast suggests the industry is entering a period of structurally higher costs rather than a short-lived squeeze. Even after memory supply stabilises, lower-end phones may not return to earlier price levels within the forecast period, according to IDC.

Nabila Popal outlined the scale of the change for both manufacturers and buyers. "The deepening memory shortage crisis remains the dominant force behind the record 14% drop this year, but it is no longer the only one," said Nabila Popal, Senior Research Director, IDC's Worldwide Quarterly Mobile Phone Tracker. "The US-Iran war has added a fresh layer of cost pressure for smartphone OEMs, driven by rising oil prices and transportation costs. Combined, these pressures are compelling vendors to reduce shipments, raise prices and concentrate on higher price tiers - elevating smartphone ASP to a record $550, up $100 from last year. 2026 will be a defining year for the industry as the new reality of structurally higher costs takes hold. For consumers, it means the era of ultra cheap smartphones is over. For vendors, it means only those that can adapt their strategies to this new cost environment and sustain demand at elevated price points will survive."

The sub-USD $100 category, which accounted for more than 170 million devices in 2025, is becoming economically unviable as memory and NAND costs settle at higher levels, IDC said. That is leaving the market increasingly concentrated among large suppliers with stronger purchasing power and better pricing control.

One area is still expanding despite the broader slump. Foldable smartphones are forecast to grow 20% year on year in 2026, making them one of the few parts of the market still increasing in both unit sales and price.

Foldables remain a small part of overall smartphone volumes, but new launches by existing manufacturers and Apple's expected entry into the category in the second half of the year are helping support growth, IDC said. The segment is also one of the few where vendors can still defend premium pricing while increasing shipments.

The overall picture points to a sharper divide between the winners and losers of the downturn. IDC expects Apple, Samsung and Huawei in China to gain share, while smaller Android brands focused on entry-level devices and emerging markets face the heaviest strain and, in some cases, may leave the market.